Main image: Slape Manor in Dorset, which came to market via Savills in September

Prime country house market snapshot: Q3 2017

Prices are still sensitive as stamp duty continues to hamper top-end country house sales, says Savills

What to read next

Middle Eastern buyers pile into the UK’s prime country house market

Knight Frank has noticed a tripling in the relative number of Middle Eastern buyers spending over £5m on English country houses...

Prime country house market slows as caution reigns

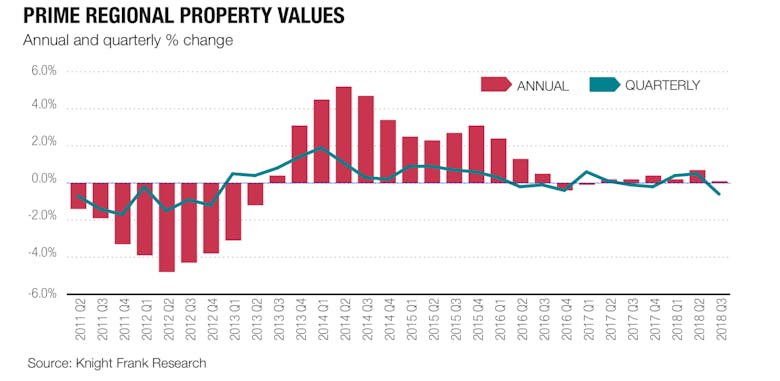

Prime regional property prices fell by an average of 0.6% in Q3, leaving the annual change at +0.1%

The prime country house market remains muted, but there are signs of pent-up demand forming

Knight Frank reports the highest number of country house buyer enquiries in five years, but price growth and stock levels are not moving

Most read

Former CBRE director launches independent advisory

Rian Strauss says international clients often have plenty of advisers, but still lack someone 'who can look across the whole situation'.

From Reel to Deal: Instagram lead ends with £16.5mn Chelsea sale

Luxury agency says social media is increasingly acting as a 'sophisticated catalyst' for big-ticket property deals.

In Pictures: Inside a £22mn Chelsea villa with one of RBKC’s last big basement builds

PCL agency lands one of the season's standout instructions in the Boltons Conservation Area.

China launches retroactive tax crackdown on wealthy citizens’ offshore assets

Beijing is said to be pursuing HNWIs for unpaid tax on overseas assets going back decades.

RBKC agency Russell Simpson expands with new SW London office

The former Head of Sales at John D Wood in Parsons Green will be leading the new operation.

Residence One tops out 29-home St John’s Wood scheme

Luxury apartment project reaches full height as developer targets May 2027 completion.

Revealed: Rightmove’s ten most viewed property listings of 2026 so far

It's an eclectic bunch, ranging from a £250k cliff-edge cottage to a £20mn Gothic mansion, via a mediaeval Scottish castle and a Victorian Manchester villa.

Family offices & bulk investors turn out for Saudi property showcase in Mayfair

Chancery Rosewood hosts second UK-Saudi exhibition as organisers claim £65.7mn of opening-day sales and reservations.

Understanding the Prime London market in five charts

From stock levels and sale prices to discounts and deal volumes, fresh graphics from LonRes provide a snapshot of the capital's prime property market as the second half of 2026 gets under way.

Agency lists Royal Tunbridge Wells’ historic town centre for sale with manorial title

'This is one of the rarest offerings to reach the UK property market in a generation,' say BNP Paribas Real Estate and Strutt & Parker.

LATEST ARTICLES

Prime London transactions up 14% as more buyers come off the sidelines

Knight Frank says buyers and sellers have become 'hardened to the volatility' as latest numbers suggest an improving picture across the prime postcodes.

Power struggle at major family-run estate agency

Boardroom rift heads to the High Court as AIM-listed firm launches proceedings against its chairman.

Prime rents climb as new rules divide the market

Rental price growth is 'stronger in markets most impacted by the Renters’ Rights Act,' says Savills, and much lower for the highest-value properties.

Record-breaking $70mn mansion sale in Silicon Valley as ‘AI investment fever’ fuels luxury market

Andrew Skurman & Suzanne Tucker-designed estate is Northern California's biggest resi deal of the year.

Required Reading: What the proposed landlord database could mean for property agents

Estate agency trade body Propertymark outlines the key points and potential fallout of some notable incoming legislation to further regulate the private rented sector.